Executive Summary

The booklet sets out the agreed revenue and capital budget set by the Combined Fire Authority at its meeting in February 2023.

The annual budget is the means by which the Authority expresses, in financial terms, its plans for service provision during the forthcoming year.

Revenue Budget

In considering its council tax requirements the Authority aims to balance the public’s requirement for and expectations of our services with the cost of providing this. As such the revenue budget focuses on the need to:

Deliver services as outlined in the Risk Management Plan and other plans.

Maintain future council tax increases at reasonable levels.

Continue to deliver efficiencies in line with targets.

Continue to invest in improvements in service delivery and facilities.

Set a robust budget that takes account of known and anticipated pressures.

Maintain an adequate level of reserves.

The Local Government Finance Settlement confirmed funding at £26.0m an increase of 6%, and that the council tax referendum level of £5.00.

The lack of a multi-year settlement makes longer term planning more difficult as there can be no certainty around future funding forecasts. Offsetting this is the opportunity provided by the £5 council tax flexibility allowed this year. The Home Office have indicated that this flexibility is only for this year.

Raising council tax by the maximum permissible still only increases the overall council tax bill by £5 but generates £2.25m of funding for the Authority. It gives greater long term funding certainty which will form the basis of our future investment requirements, which are essential if we are to hit our ‘road to outstanding’ ambition and be the best equipped, best trained and best accommodated Service.

The final proposed revenue budget for 2023/24 is £68.2m, an increase of 8%. This results in a council tax requirement of £8227 per Band D property, an increase of £5.00 per annum (less than 10p per week).

Until such time as the outcome of next year’s Spending review is published it is impossible to provide any meaningful funding forecast, however for the purpose of medium-term financial planning we have assumed that funding is increased by 5.0% next year and 2% thereafter, and the council tax referendum principle returns to its standard 3%.

Based on this, and the other assumptions within the budget, the Authority is able to deliver a balanced budget in future years, utilising a combination of further savings and drawdown of reserves.

Looking at the medium-term plans it is clear that the key variables remain pay awards, pension costs and funding. Any significant increase in pay award over and above those built into the budget or in the cost of FF pensions will add in significant financial pressures. Similarly, should funding settlements be worse than budgeted then the level of deficit will increase accordingly.

The Authority remains in a good financial position.

Capital Strategy/Budget

In terms of the Authority’s Capital Programme our capital strategy is designed to ensure that the Authorities capital investment:

Assists in delivering the corporate objectives.

Provides the framework for capital funding and expenditure decisions, ensuring that capital investment is in line with priorities identified in asset management plans.

Ensures statutory requirements are met, i.e. Health and Safety issues.

Supports the Medium-Term Financial Strategy by ensuring all capital investment decisions consider the future impact on revenue budgets.

Demonstrates value for money in ensuring the Authority’s assets are enhanced/preserved.

Describes the sources of capital funding available for the medium term and how these might be used to achieve a prudent and sustainable capital programme.

In light of this, the capital budget continues to invest in our asset base, in particular vehicle replacement, refurbishment/replacement of stations, potential relocation of Headquarters, new IT requirements and new operational equipment. This gives rise to a capital program of £55m over the next five years.

Whilst the programme over the next five years requires £11m of borrowing, this is accounted for in the revenue budget, and hence the capital programme is considered affordable, prudent and sustainable.

Reserves and Balances

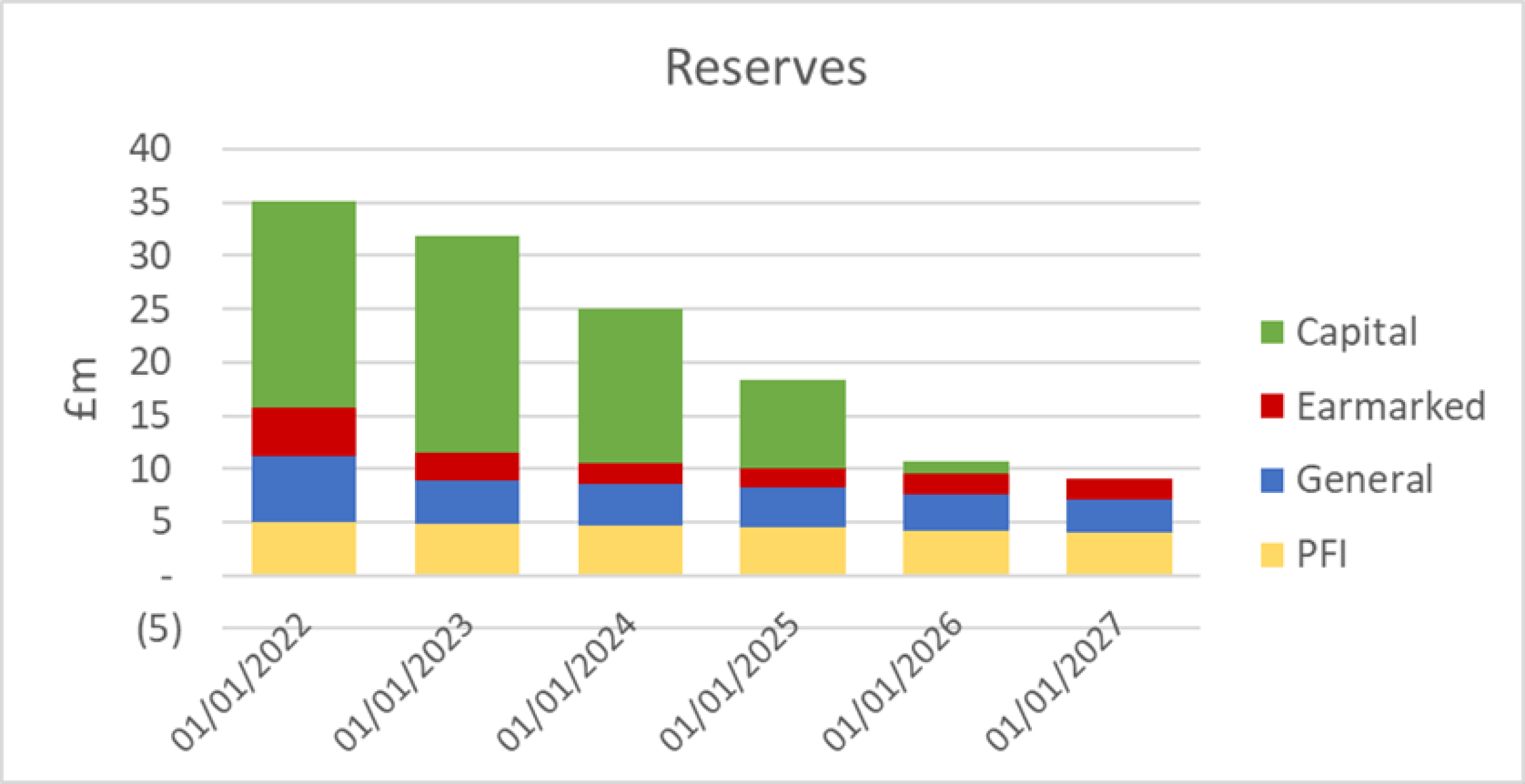

In terms of reserves and balances, the Authority has identified a General Reserves minimum target of £3.75m and a maximum target of £10.0m. After allowing for the anticipated usage the Authority estimates it will hold £4.0m of uncommitted reserves by 31 March 2023. The revenue budget identifies a need to utilise £0.15m of these in 23/24, leaving a balance of £3.85m, in excess of the minimum level, and hence the Treasurer considers these are adequate to meet our requirements.

Other reserves reduce significantly over the 5 year plan, reflecting their utilisation to support the capital programme.

Treasury Management

The Treasury Management strategy shows the Authority holding surplus cash, which is available for investment or to pay off existing debt. However, given the penalty associated with debt repayment, and the future need to borrow, it is not considered appropriate to pay off debt at this point in time.

Section 1: Revenue Budget

In line with the Authority’s objective to deliver affordable, value for money services the Authority’s Budget Strategy remains one of:

Maintaining future council tax increases at reasonable levels, reducing if possible.

Continuing to deliver efficiencies in line with targets.

Continuing to invest in improvements in service delivery.

Continuing to invest in improving facilities.

Setting a robust budget.

Maintaining an adequate level of reserves.

Budget

In order to determine the future budget requirement, the Authority has used the approved 2022/23 budget as a starting point, and has uplifted this for inflation and other known changes and pressures, to arrive at a draft budgetary requirement, prior to utilising any reserves, as set out below:

Summary of Budget Changes

Summary | 2023/24 £m | 2024/25 £m | 2025/26 £m | 2026/27 £m | 2027/28 £m |

|---|---|---|---|---|---|

Preceding Years Draft Net Budget Requirement | 63.0 | 68.5 | 71.8 | 74.5 | 76.6 |

Add back previous years unidentified savings target | – | – | – | – | – |

Add back previous years Vacancy Factors | 1.6 | 1.8 | 1.4 | 0.6 | 0.7 |

Inflation | 7.5 | 2.0 | 1.7 | 1.7 | 1.7 |

Other Pay Pressures | (0.7) | 0.7 | – | – | – |

Committed Variations | 0.5 | 0.3 | 0.3 | 0.3 | 0.3 |

Growth | 0.2 | – | – | – | – |

Efficiency Savings | (1.9) | – | 0.1 | 0.1 | 0.1 |

Gross Budget Requirement | 70.3 | 73.2 | 75.1 | 77.3 | 79.6 |

Vacancy Factors | (1.8) | (1.4) | (0.6) | (0.7) | (0.7) |

Net Budget Requirement | 68.5 | 71.8 | 74.5 | 76.6 | 78.9 |

Unidentified Savings/drawdown of Reserves to balance 23/24 Budget | (0.3) | ||||

68.2 | 71.8 | 74.5 | 76.6 | 78.9 |

Inflation

The following amounts have been added to the budget in respect of inflationary pressures, in line with current estimates:

Details of Inflation

Summary | 2023/24 £m | 2024/25 £m | 2025/26 £m | 2026/27 £m | 2027/28 £m |

|---|---|---|---|---|---|

The impact of the unbudgeted pay awards in 2022/23:

| 2.5 | – | – | – | – |

A 5% allowance has been built in for 2023/24 pay award and 2% thereafter. | 2.4 | 1.5 | 1.2 | 1.2 | 1.2 |

The budget allows for a general 10% inflationary increase next year in respect of non-pay, split across underfunded inflation in 22/23 and an assumed 5% inflation in 23/24. With on-going inflation of 2.5% thereafter. In addition the on-going budget for energy and fuel has been increased to reflect current rates. | 2.6 | 0.5 | 0.5 | 0.5 | 0.5 |

7.5 | 2.0 | 1.7 | 1.7 | 1.7 |

Each 1% pay award in excess of the above assumptions equates to an additional cost of £0.4m per year for grey book personnel, and £0.1m for green book personnel.

Other Pay Pressures

Details of Other Pay Pressures

Summary | 2023/24 £m | 2024/25 £m | 2025/26 £m | 2026/27 £m | 2027/28 £m |

|---|---|---|---|---|---|

Pay has been re-costed, taking account of changes to personnel, grades, public holidays, pension costs etc. | (0.3) | (0.1) | – | 0.1 | – |

Removal of the Employers National Insurance increase of 1.25% in relation to the Health and Social Care levy. | (0.4) | – | – | – | – |

The 2020 valuation exercise on the Fire Fighters pension is on-going, with any changes arising from this anticipated to impact the 2024/25. It is not clear what impact this will have but we are likely to see an increase in employer contribution rates, the scale of which is, as yet, unknown. Therefore we have assumed a 3% increase in the 24/25 budget, pending further clarification. | – | 0.8 | – | – | – |

(0.7) | 0.7 | – | 0.1 | – |

Committed Variations

Committed variations are those items which are unavoidable, or which arise from previously agreed policy decisions.

Details of Committed Variations

Summary | 2023/24 £m | 2024/25 £m | 2025/26 £m | 2026/27 £m | 2027/28 £m |

|---|---|---|---|---|---|

The budget reflects the reduction in the drawdown against the apprentice levy, net of our 5% co-investment cost, due to the reduction in future FF recruit numbers. | – | 0.2 | 0.1 | 0.1 | – |

The budget for pooled PPE has been adjusted in future years to reflect lifecycle replacement requirement, which see a significant increase in 25/26 and beyond reflecting the age profile of our existing stock. | – | – | 0.2 | (0.1) | 0.2 |

The budget for operational equipment has been adjusted in future years to reflect lifecycle replacement requirement. | 0.1 | – | – | 0.2 | (0.2) |

The following budgets have been increased to reflect a combination of cost pressures and increased demand:

| 0.3 | – | – | – | – |

The budget for NWFC has been increased to reflect cost pressures within the function, which are passed on to the relevant Authorities, our share of these being 25%. NWFC are commencing a project to replace the mobilizing software, and whilst some project costs are included in the above pressures, this does not include any allowance for the eventual cost of the replacement software, which is likely to be a very significant cost. Hence the cost in future years is likely to increase further, but as yet we have no details. | 0.1 | – | – | – | – |

The increased capital financing charge in 27/28 reflects borrowing requirements associated with the capital programme (as referred to in the Capital budget report elsewhere on the agenda) | – | – | – | – | 0.3 |

Other | – | 0.1 | – | 0.1 | – |

0.5 | 0.3 | 0.3 | 0.3 | 0.3 |

Growth

Details of Growth

Summary | 2023/24 £m | 2024/25 £m | 2025/26 £m | 2026/27 £m | 2027/28 £m |

|---|---|---|---|---|---|

There have been some increases in budget relating to specialist functions, such as the Drone Team and our Canine Teams | 0.2 | – | – | – | – |

0.2 | – | – | – | – |

Efficiency Savings

The Authority has a good track record of delivering efficiency savings, with the following savings identified below:

Details of Efficiency Savings

Summary | 2023/24 £m | 2024/25 £m | 2025/26 £m | 2026/27 £m | 2027/28 £m |

|---|---|---|---|---|---|

The outcome of the ECR delivers total savings of £0.4m, with phasing as shown | (0.5) | 0.2 | (0.1) | – | – |

The budget allows for the following recruits/apprentice FFs each year:

These forecasts take account of the timing of changes to establishment, predominantly arising from the outcome of the ECR, as well anticipated retirements/early levers. However, it should be noted that the timing and number of retirements/early leavers has varied significantly in recent years. | (0.2) | (0.3) | – | – | – |

A number of temporary posts will be removed in future years | – | (0.3) | (0.1) | (0.1) | – |

Interest receivable has increased in 23/24, reflecting the change in bank base rates, and the increased use of fixed term deposits. This gradually reduces over the life of the strategy, reflecting the reduction in cash balances and falling interest rates in future years | (1.0) | 0.4 | 0.3 | 0.2 | 0.1 |

Other | (0.2) | – | – | – | – |

(1.9) | – | 0.1 | 0.1 | 0.1 |

Gross Budget Requirement

As set out above the overall gross budget requirement for each year is as follows:

Gross Budget Requirement

Summary | 2023/24 £m | 2024/25 £m | 2025/26 £m | 2026/27 £m | 2027/28 £m |

|---|---|---|---|---|---|

Draft Gross Budget Requirement | 70.3 | 73.2 | 75.1 | 77.3 | 79.6 |

Vacancy Factors

The budget needs to take account of forecast vacancy factors arising from retirement and recruitment profiles:

Details of Vacancy Factors

Summary | 2023/24 £m | 2024/25 £m | 2025/26 £m | 2026/27 £m | 2027/28 £m |

|---|---|---|---|---|---|

The vacancy/over establishment factor for whole-time has also been updated and is based on the following:

Overall, this results in a net under-establishment in 23/24, a broadly balanced position in 24/25 and a net over-establishment in 25/26 and beyond. It should be noted that any vacancies are partly offset by a potential increase in overtime costs. | (0.3) | (0.2) | 0.3 | 0.1 | 0.1 |

On Call vacancy factors have been increased from 21% to 25% reflecting the current level of staffing. However we have assumed that this reduces in future years, reflecting our desire to improve our recruitment and retention of on call personnel, reducing to 15% by 27/28. | (0.8) | (0.7) | (0.7) | (0.6) | (0.5) |

Support staff vacancy factor has been set at 7.5% in 23/24, lower than its current level; on the assumption that we are successful in our current recruitment campaigns. We have reduced this in subsequent years, down to 2.5% by 25/26. | (0.7) | (0.5) | (0.2) | (0.2) | (0.3) |

(1.8) | (1.4) | (0.6) | (0.7) | (0.7) |

Net Budget Requirement

As set out above the overall net budget requirement for each year is as follows:

Net Budget Requirement

Summary | 2023/24 £m | 2024/25 £m | 2025/26 £m | 2026/27 £m | 2027/28 £m |

|---|---|---|---|---|---|

Draft Budget Requirement | 68.5 | 71.8 | 74.5 | 76.6 | 78.9 |

Budget Increase | 8.7% | 4.8% | 3.9% | 2.8% | 2.9% |

Proposed Budget Requirement

In order to balance to available funding in 2023/24 a further £0.3m of budget reductions are required, as referred to later in the report. This gives a revised budget requirement in 202/24 of £68.2m.

Proposed Budget Requirement

Summary | 2023/24 | 2024/25 | 2025/26 | 2026/27 | 2027/28 |

|---|---|---|---|---|---|

Draft Budget Requirement | 68.5 | 71.8 | 74.5 | 76.6 | 78.9 |

Additional Saving/drawdown of reserve | (0.3) | – | – | – | – |

Final Proposed Budget | 68.2 | 71.8 | 74.5 | 76.6 | 78.9 |

Budget Increase | 8.2% | 5.3% | 3.9% | 2.8% | 2.9% |

Analysis of Budget by Service Area

Budget by Service Area

Service Area | 2023/24 Budget £m | 2024/25 Budget £m | 2025/26 Budget £m | 2026/27 Budget £m | 2027/28 Budget £m |

|---|---|---|---|---|---|

Service Delivery | 39.223 | 41.090 | 42.520 | 43.404 | 44.402 |

Prevention and Protection | 3.210 | 3.383 | 3.475 | 3.551 | 3.627 |

Control | 1.610 | 1.671 | 1.734 | 1.799 | 1.866 |

Special Projects | 0.036 | 0.037 | 0.037 | 0.038 | 0.038 |

Service Development | 1.962 | 2.048 | 2.111 | 2.155 | 2.199 |

Training | 4.571 | 4.456 | 4.673 | 4.882 | 5.066 |

Fleet Services | 3.282 | 3.403 | 3.461 | 3.748 | 3.581 |

ICT | 3.330 | 3.415 | 3.519 | 3.608 | 3.699 |

Digital Transformation | 0.609 | 0.635 | 0.662 | 0.625 | 0.638 |

Human Resources | 1.071 | 1.119 | 1.093 | 1.116 | 1.139 |

Occupational Health | 0.318 | 0.330 | 0.342 | 0.350 | 0.357 |

Corporate Communications | 0.386 | 0.403 | 0.420 | 0.429 | 0.438 |

Health & Safety | 0.288 | 0.299 | 0.311 | 0.318 | 0.324 |

Executive Board | 1.124 | 1.177 | 1.211 | 1.236 | 1.261 |

Central Admin Hub | 0.955 | 0.999 | 1.045 | 1.067 | 1.088 |

Finance | 0.221 | 0.231 | 0.242 | 0.247 | 0.252 |

Procurement | 0.667 | 0.676 | 0.907 | 0.856 | 1.080 |

Property | 4.012 | 4.120 | 4.232 | 4.338 | 4.448 |

Pensions Expenditure | 1.399 | 1.475 | 1.480 | 1.547 | 1.619 |

Other Non-DFM Expenditure | 0.219 | 0.791 | 1.073 | 1.331 | 1.754 |

Gross Budget Requirement | 68.493 | 71.757 | 74.548 | 76.642 | 78.876 |

Unidentified Savings/Use of Reserves | (0.310) | ||||

Net Budget Requirement | 68.183 | 71.757 | 74.548 | 76.642 | 78.876 |

Analysis of Budget by Type of Expenditure

Summary | 2023/24 Budget £m | 2024/25 Budget £m | 2025/26 Budget £m | 2026/27 Budget £m | 2027/28 Budget £m |

|---|---|---|---|---|---|

Employee | |||||

Uniformed | 43.871 | 45.877 | 47.228 | 48.158 | 49.234 |

Support staff | 8.976 | 9.161 | 9.493 | 9.654 | 9.870 |

Pensions | 1.392 | 1.468 | 1.473 | 1.540 | 1.612 |

Other Employee Related Exp | 0.064 | 0.065 | 0.067 | 0.069 | 0.070 |

54.303 | 56.571 | 58.261 | 59.421 | 60.786 | |

Premises | |||||

R&M | 1.235 | 1.265 | 1.297 | 1.329 | 1.362 |

Utilities | 1.821 | 1.866 | 1.913 | 1.960 | 2.009 |

Cleaning | 0.070 | 0.071 | 0.073 | 0.074 | 0.076 |

PFI | 0.743 | 0.761 | 0.780 | 0.800 | 0.820 |

Other | 0.062 | 0.064 | 0.065 | 0.067 | 0.068 |

Rent/Rates | 1.415 | 1.485 | 1.558 | 1.635 | 1.717 |

5.344 | 5.512 | 5.686 | 5.866 | 6.052 | |

Transport | |||||

Repairs | 0.950 | 0.974 | 0.998 | 1.023 | 1.048 |

Running Costs | 0.590 | 0.605 | 0.620 | 0.635 | 0.651 |

Travel costs | 0.486 | 0.498 | 0.511 | 0.523 | 0.536 |

insurance | 0.244 | 0.250 | 0.256 | 0.263 | 0.269 |

Other | 0.006 | 0.006 | 0.006 | 0.006 | 0.006 |

2.276 | 2.333 | 2.390 | 2.450 | 2.511 | |

Supplies & Services | |||||

Hydrants | 0.082 | 0.084 | 0.086 | 0.088 | 0.090 |

Operational equipment | 0.785 | 0.825 | 0.805 | 1.030 | 0.799 |

Clothing & Uniform | 0.488 | 0.483 | 0.700 | 0.645 | 0.865 |

Printing, stationery, postage | 0.519 | 0.531 | 0.544 | 0.558 | 0.571 |

Comms-Network Costs | 1.178 | 1.208 | 1.238 | 1.269 | 1.300 |

Telephony | 0.221 | 0.227 | 0.233 | 0.238 | 0.244 |

Computers | 1.684 | 1.726 | 1.769 | 1.814 | 1.859 |

Subsistence | 0.105 | 0.108 | 0.110 | 0.113 | 0.115 |

Fire Safety Expenses | 0.332 | 0.341 | 0.349 | 0.358 | 0.367 |

Training Expenses | 0.505 | 0.517 | 0.530 | 0.543 | 0.557 |

insurance | 0.280 | 0.285 | 0.291 | 0.297 | 0.303 |

Members Expenses | 0.193 | 0.197 | 0.202 | 0.207 | 0.212 |

Misc Equipment | 0.099 | 0.101 | 0.104 | 0.106 | 0.109 |

Other | 1.401 | 1.590 | 1.777 | 2.055 | 2.172 |

Catering | 0.094 | 0.097 | 0.099 | 0.102 | 0.104 |

PTV Residential | 0.108 | 0.110 | 0.113 | 0.116 | 0.119 |

8.074 | 8.431 | 8.950 | 9.537 | 9.787 | |

Other | |||||

Contracted Services | 1.274 | 1.357 | 1.380 | 1.311 | 1.344 |

Other | 0.004 | 0.004 | 0.005 | 0.005 | 0.005 |

1.278 | 1.362 | 1.384 | 1.316 | 1.348 | |

Capital Financing Costs | 4.100 | 4.100 | 4.100 | 4.100 | 4.400 |

Income | (6.882) | (6.552) | (6.223) | (6.046) | (6.007) |

Gross Budget Requirement | 68.493 | 71.757 | 74.548 | 76.642 | 78.876 |

Unidentified Savings/Use of Reserves | (0.310) | 0.000 | 0.000 | 0.000 | 0.000 |

Net Budget Requirement | 68.183 | 71.757 | 74.548 | 76.642 | 78.876 |

Revenue Funding 2023/24-2027/28

Grant Funding

The Government’s Budget will set the overall total for public sector spending which will then be allocated out to departments as part of the Spending Review, and these are then allocated out to individual Authorities as part of the Local Government Finance Settlement, the final version being announced on 6 February.

Due to economic uncertainty the anticipated multi-year settlement has been postponed again, hence the draft settlement only covers 23/24.

Similarly, the Fair Funding review, which looked to re-assess the methodology under which funding was allocated to individual authorities, and the implementation of a revised Business Rates Retention Scheme, have both been put on hold for at least a further 12 months.

The 2023/24 Local Government Finance Settlement showed an increase in the Government’s Settlement Funding Assessment of 6.05%. The Settlement Funding Assessment comprises:

Details of Settlement Funding Assessment 2023/24

Summary | Total |

|---|---|

Revenue Support Grant (from the Government) | £9.7m |

Business Rates (from local billing authorities) | £11.6m |

Business Rates Top-Up (from the Government) | £4.7m |

Total | £26.0m |

Looking beyond 23/24, the policy statement that accompanied the finance settlement stated “The core settlement will continue in a similar manner for 2024-25. The major grants will continue as set out for 2023-24: Revenue Support Grant will continue and be uplifted in line with Baseline Funding Levels”. We have therefore assumed that the settlement funding assessment will grow in line with inflation in 24/25 (assumed to be 5.0%) and thereafter by 2.0% (the Governments inflation target). The table below sets out our assumed level of funding (Settlement Funding Assessment) over the next 5 years:

Forecast Settlement Funding Assessment 2023/24-2027/28

Summary | 2023/24 £m | 2024/25 £m | 2025/26 £m | 2026/27 £m | 2027/28 £m |

|---|---|---|---|---|---|

Estimated Settlement Funding Assessment | 26.0 | 27.3 | 27.8 | 28.4 | 29.0 |

Growth | 6.0% | 5.0% | 2.0% | 2.0% | 2.0% |

Service Grant

The Service Grant has been reduced to 0.6m, reflecting the removal of the elements relating to the increase in employer National Insurance Contributions identified last year, but which has now been reversed.

Forecast Service Grant

Summary | 2023/24 £m | 2024/25 £m | 2025/26 £m | 2026/27 £m | 2027/28 £m |

|---|---|---|---|---|---|

Service Grant | 0.6 | 0.6 | 0.6 | 0.6 | 0.6 |

Business Rates Adjustments

We have received final details of Business Rates from billing authorities, confirming that our local retention of business rates at £4.3m, £0.4m than allowed for in the settlement above.

In addition to the above Business Rates the Authority receives Section 31 grant from the Government to compensate for specific reliefs it has agreed as part of policy decisions, i.e. small business relief etc. This year the anticipated grant has increased to £3.9m, reflecting the higher Government multiplier being applied this year. We have assumed these increases in line with inflation in future years.

Billing Authorities have conformed an overall surplus on the collection fund of £133k. Given the volatility of this we have assumed a breakeven position I future years.

Forecast Business Rates Adjustments

Summary | 2023/24 £m | 2024/25 £m | 2025/26 £m | 2026/27 £m | 2027/28 £m |

|---|---|---|---|---|---|

Local Business Rate adjustment, as per Billing Authorities | (0.4) | (0.4) | (0.4) | (0.4) | (0.4) |

Section 31 Grant – Business Rates Reliefs | 3.9 | 4.0 | 4.1 | 4.2 | 4.3 |

Business Rates Collection Fund Surplus | 0.1 | – | – | – | – |

Total Business Rates Adjustment | 3.6 | 3.6 | 3.7 | 3.8 | 3.9 |

Council Tax

In setting the council tax, the Authority aims to balance the public’s requirement for our services with the cost of providing this. As such the underlying principle of any increase in council tax is that this must be seen as reasonable within the context of service provision.

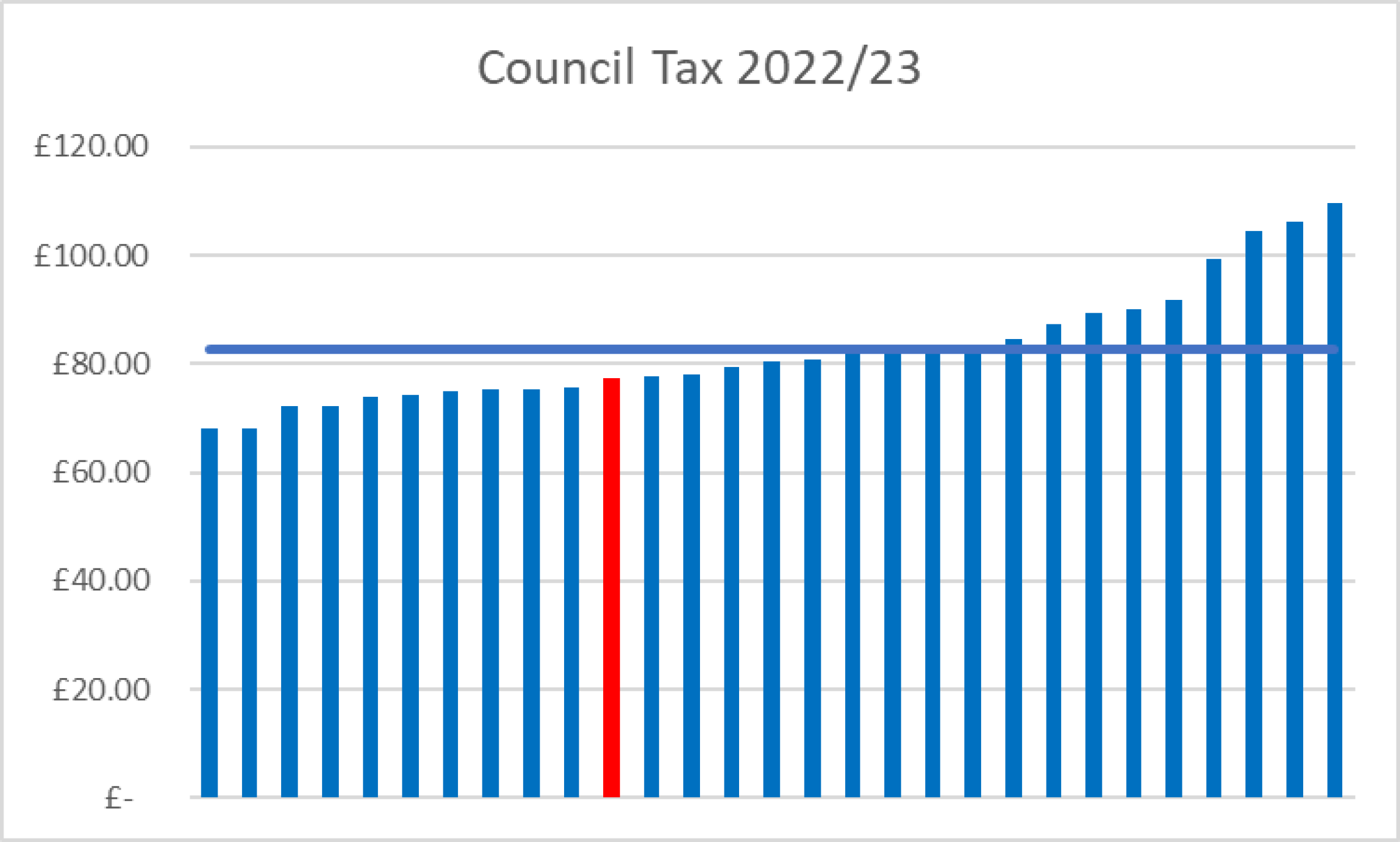

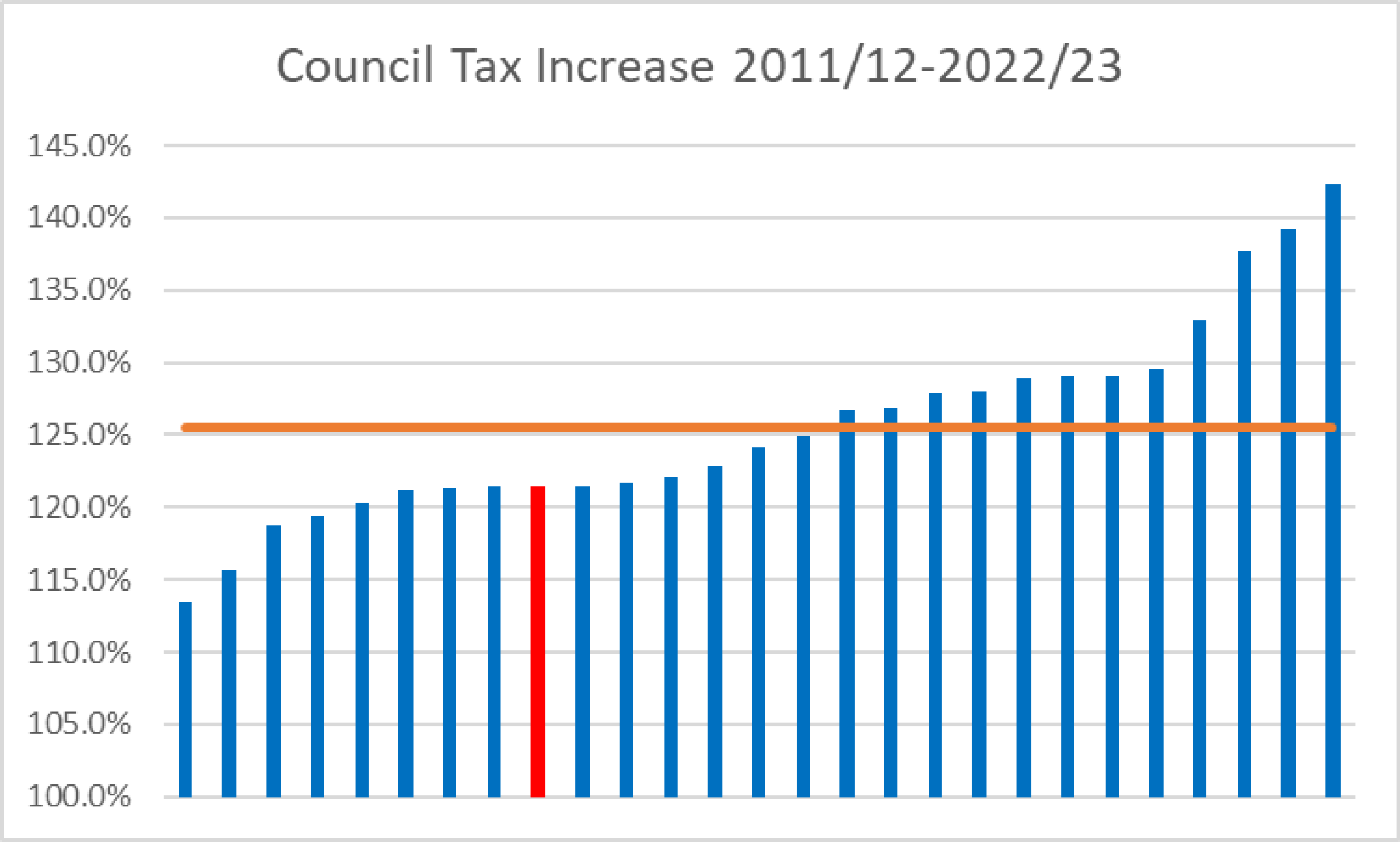

The Authority became a precepting authority on 1 April 2004. Since this our council tax increases have been limited by either capping or the current referendum thresholds set by the Government. As such our council tax increases and hence budget increases have been constrained by these and our desire to deliver value for money services. Last year the Government allowed the 8 FRAs with the lowest precept levels to increase council tax by £5, with Lancashire being one of the Authorities that took advantage of this flexibility. Despite this our council tax of £77.27 is still below the national average of £82.65, and our increase of just 21.4% since 2010/11 compares with an average increase of 25.5% over the same period.

Graph 1 Comparative Council Tax 2022/23

Graph 2 Comparative Council Tax Cumulative Increase 2011-2023

The Local Government Settlement confirmed that the Government setting a 3% core referendum threshold, whilst allowing all Fire Authorities to increase council tax by £5 for one year only in 2023/24. It is worth highlighting that prior to last year this flexibility had not been granted since 2013/14. Furthermore, the Government has confirmed that at the present time its intention is for the 3% referendum threshold to be applied in 24/25.

An increase of £5 would result in a council tax of £82.27 per band D property. Based on our estimated tax base this will generate £2.3m of funding compared with £1.1m from a 3% increase, an additional £1.2m. Furthermore, it should be emphasised that this additional funding will set a new council tax baseline and hence becomes a recurring increase.

Council Tax-Base

The Authorities council tax-base has increased by 1.8% in 23/24. For the purpose of medium term forecasting we have assumed that the taxbase increases by 1.5% in subsequent years in line with historic averages.

Forecast Council Tax-Base

Summary | 2023/24 | 2024/25 | 2025/26 | 2026/27 | 2027/28 |

|---|---|---|---|---|---|

Estimated Number of Band D equivalent properties | 457,949 | 464,819 | 471,791 | 478,868 | 486,051 |

Billing Authorities have now confirmed on overall collection fund surplus is £275k. We have assumed a £400k surplus on the collection fund each, in line with historic averages in future years:

Forecast Council Tax Collection Fund

Summary | 2023/24 £m | 2024/25 £m | 2025/26 £m | 2026/27 £m | 2027/28 £m |

|---|---|---|---|---|---|

Council Tax Collection Surplus | 0.3 | 0.4 | 0.4 | 0.4 | 0.4 |

Draft Council Tax Requirements

Forecast Council Tax Requirements

Summary | 2023/24 £m | 2024/25 £m | 2025/26 £m | 2026/27 £m | 2027/28 £m |

|---|---|---|---|---|---|

Draft Budget Requirement | 68.5 | 71.8 | 74.5 | 76.6 | 78.9 |

Less Settlement Funding Assessment | (26.0) | (27.3) | (27.8) | (28.4) | (29.0) |

Less Service Grant | (0.6) | (0.6) | (0.6) | (0.6) | (0.6) |

Less Business Rates Adjustment | (3.6) | (3.6) | (3.7) | (3.8) | (3.9) |

Less Council Tax Collection Surplus | (0.3) | (0.4) | (0.4) | (0.4) | (0.4) |

Equals Precept | 38.0 | 39.8 | 41.9 | 43.4 | 45.0 |

Estimated Number of Band D equivalent properties | 457,949 | 464,819 | 471,791 | 478,868 | 486,051 |

Equates to Council Tax Band D Property | £82.95 | £85.55 | £88.87 | £90.60 | £92.51 |

Increase in Council Tax | 7.3% | 3.1% | 3.9% | 1.9% | 2.1% |

(For information, a 1% change to the council tax equates to £0.35m.)

As can be seen the increases in 23/24, 24/25 and 25/26 are all above the referendum thresholds. As such the Authority will need to reduce its budget requirement in these years in order to deliver a balanced budget within the referendum thresholds:

Budget Reductions Required

Summary | 2023/24 £m | 2024/25 £m | 2025/26 £m | 2026/27 £m | 2027/28 £m |

|---|---|---|---|---|---|

Budget reduction required | 0.3 | 0.4 | 0.8 | 0.3 | – |

The Authority can achieve this by either utilising reserves, identifying additional savings or a combination of both.

Reserves

A reasonable level of reserves is needed to provide an overall safety net against unforeseen circumstances, such as levels of inflation/pay awards in excess of budget provision, unanticipated expenditure on major incidents, and other “demand led” pressures, such as increased pension costs, additional costs associated with national projects, etc. which cannot be contained within the base budget. In addition, they also enable the Authority to provide for expenditure, which was not planned at the time the budget was approved, but which the Authority now wishes to implement.

As such a review of the strategic, operational and financial risk facing the Authority is undertaken each year to identify an appropriate level of reserves to hold, this incorporates issues such as higher than anticipated inflation, including pay awards, increased pension costs, particularly those arising from McCloud Sergeant, successful implementation of the ECR, and costs associated with potential industrial action. given the latest pay offer and the Finance Settlement policy Statements indication about future funding, the treasurer recommends reducing the minimum requirement to £3.75m. As at 31 March 2023 we anticipate holding £4.0m, providing scope to utilise approx. £0.25m of reserves. (Note, it may be possible to reduce this minimum level further if the current grey book 2 year pay offer is accepted).

Therefore, the Treasurer considers this reserve is at an appropriate level.

Robustness of the Revenue Budget 2023/24

Under Section 25 of the Local Government Act 2003, the Chief Finance Officer is required to make a statement about the robustness of the budget.

The professional opinion of the Treasurer is that the budget has been prepared on a robust basis for the following reasons:

The budget is reflective of existing service plans;

The budget takes account of the anticipated on-going revenue impact of current and future capital programmes;

The allowances included for inflation and pay awards represent a best estimate of the likely cost of this, as set out below:

Inflationary Allowance Included in Budget

Summary | 2023/24 |

|---|---|

Uniformed Pay Award (7% backdated pay award allowed for 22/23) | 5.0% |

Non-Uniformed Pay Award | 5.0% |

Non-Pay Inflation (In addition to the backdated adjustments to reflect inflation levels in 22/23) | 5.0% |

As part of the budget setting process all estimates, including savings and income forecast, are assessed for reasonableness;

The situation in respect of future funding, and in particular the outcome of next year’s Local Government Finance Settlement and any subsequent Spending Review will be kept under review and reported to the Authority in due course.

The level of and appropriateness of reserves has been reviewed by the Treasurer, based on the potential risks faced by the Authority;

The following significant financial risks have all been assessed and the Treasurer feels that these are adequately covered within the budget estimates presented or within the level of reserves currently held:

Reductions in funding levels over and above those forecast;

Reduction in funding via Business Rates retention scheme;

Reduction in council tax funding due to changes in collection rates, localisation of council tax support, reducing tax base and/or council tax referendum limits;

Higher than anticipated inflation;

Larger increases in future pension costs/contributions;

Significant changes in retirement profiles;

Increase in costs arising from demand led pressures, i.e., increasing staff numbers, overtime due to spate conditions or major equipment replacement requirements;

Inadequacy of insurance arrangements.

Summary Council Tax 2022/23

We are recommending a £5.00 increase in council tax for an average band D property:-

Detailed Council Tax Requirement 2023/24

Summary | £m |

|---|---|

Gross Budget Requirement | 68.5 |

Less Budget reduction required | (0.3) |

Net Budget Requirement | 68.2 |

Less Settlement Funding Assessment | (26.0) |

Less Service Grant | (0.6) |

Less Business Rates Adjustment | (3.6) |

Less Council Tax Collection Surplus | (0.3) |

Equals Precept | 37.7 |

Estimated Number of Band D equivalent properties | 457,949 |

Equates to Council Tax Band D Property | £82.27 |

Increase in Council Tax | £5.00 |

The increase of £5.00 per annum equating to 10p per week for an average band D property.

It is also worth highlighting that Fire accounts for a very small proportion of the total council tax bill, with the 2022/23 average band D bill in Lancashire being £2,075, of which ‘Fire’ accounts for £77, less than 4%.

Graph 3 Council Tax in Lancashire 2022/23

Summary and Conclusions

The lack of a multi-year settlement makes longer term planning more difficult as there can be no certainty around future funding forecasts. Offsetting this is the opportunity provided by the £5 council tax flexibility allowed this year

Raising council tax by the maximum permissible still only increases the overall council tax bill by £5 but generates £2.3m of funding for the Authority. It is proposed to utilise a combination of drawdown from reserves and further savings to bridge funding gap in 23/24 and beyond, the extent of this requirement being dependant upon final pay award agreement and future funding settlements.

As proposed the council tax increase/budget gives greater long term funding certainty which will form the basis of our future investment requirements (as reflected in the Medium Term Financial Strategy and the Capital Programme), which are essential if we are to hit our ‘road to outstanding’ ambition and be the best equipped, best trained and best accommodated Service.

Whilst the council tax is expressed as a Band D equivalent figure, there are actually 8 property bandings, each of which has a council tax set in proportion to the band D figure (i.e. a band A property is 2/3rds that of a band D charge, and band H is twice that of a band D charge). The individual Council Tax bandings are set out below:

Council Tax by Band

Band | Charge |

|---|---|

Band A | £54.85 |

Band B | £63.99 |

Band C | £73.13 |

Band D | £82.27 |

Band E | £100.55 |

Band F | £118.83 |

Band G | £137.12 |

Band H | £164.54 |

Section 2: Capital Budget

Capital Strategy/Budget 2023/24-2027/28

Capital Budget Strategy

The Authority’s capital strategy is designed to ensure that the Authority’s capital investment:

Assists in delivering the corporate objectives.

Provides the framework for capital funding and expenditure decisions, ensuring that capital investment is in line with priorities identified in asset management plans.

Ensures statutory requirements are met, i.e. Health and Safety issues.

Supports the Medium-Term Financial Strategy by ensuring all capital investment decisions consider the future impact on revenue budgets.

Demonstrates value for money in ensuring the Authority’s assets are enhanced/preserved

Describes the sources of capital funding available for the medium term and how these might be used to achieve a prudent and sustainable capital programme.

Managing capital expenditure

The Capital Programme is prepared annually through the budget setting process and is reported to the Authority for approval each February. The programme sets out the capital projects taking place in the financial years 2023/24 to 2027/28 and will be updated in May to reflect the effects of the final level of slippage from the current financial year (2022/23).

The majority of projects originate from approved asset management plans, subject to assessments of ongoing requirements. Bids for new capital projects are evaluated and prioritised by Executive Board prior to seeking Authority approval.

A budget manager is responsible for the effective financial control and monitoring of their elements of the capital programme. Quarterly returns are submitted to the Director of Corporate Services on progress to date and estimated final costs. Any variations are dealt with in accordance with the Financial Regulations (Section 4.71). Where expenditure is required or anticipated which has not been included in the capital programme, a revision to the Capital Programme must be approved by Resources Committee before that spending can proceed.

Proposed Capital Budget

Capital expenditure is expenditure on major assets such as new buildings, significant building modifications and major pieces of equipment/vehicles.

The Service has developed asset management plans which assist in identifying the long-term capital requirements. These plans, together with the operational equipment register have been used to assist in identifying total requirements and the relevant priorities.

Vehicles

The Fleet Asset Management plan has been used as a basis to identify the following vehicle replacement programme, which is based on current approved lives:

Vehicle Requirements (Numbers and cost by type per year)

Type of Vehicle | 2023/24 | 2024/25 | 2025/26 | 2026/27 | 2027/28 |

|---|---|---|---|---|---|

Pumping Appliance | 13 | – | 3 | 6 | 11 |

Climate Change Vehicle | 2 | – | – | – | – |

Command Unit | 3 | – | – | – | – |

Water Tower | 2 | – | – | – | – |

Aerial appliance | 1 | – | – | – | – |

All-Terrain Vehicle | 1 | – | – | – | – |

Prime mover | 2 | – | – | – | – |

Pod | 3 | – | – | – | 1 |

Operational Support Vehicles | 37 | 20 | 12 | 16 | 18 |

64 | 20 | 15 | 22 | 30 | |

Budget (£m) | |||||

Pumping Appliance | 1.930 | – | 0.660 | 1.320 | 2.420 |

Climate Change Vehicle | 0.500 | – | – | – | – |

Command Unit | 0.715 | – | – | – | – |

Water Tower | 1.027 | – | – | – | – |

Aerial appliance | 0.534 | – | – | – | – |

All-Terrain Vehicle | 0.018 | – | – | – | – |

Prime mover | 0.260 | – | – | – | – |

Pod | 0.083 | – | – | – | 0.030 |

Operational Support Vehicles | 1.030 | 0.678 | 0.315 | 0.512 | 0.584 |

6.097 | 0.678 | 0.975 | 1.832 | 3.034 |

(Note several of the vehicles shown in 23/24 have already been ordered and are subject to phased payment, hence the cost shown is the element which is due in 23/24).

Numbers are based on order date. Several of the vehicles have long lead times, and stage payments, hence the actual timing of spend is subject to change, with any deliveries spanning across years inevitably resulting in the need to move spend between years, usually this will be in the form of slippage into subsequent years, but occasionally there will be a need to pull budget forward to reflect an earlier delivery/stage completion date. This will be reported to Resources Committee as delivery dates are agreed.

All vehicles are replacements for existing vehicles, although in the case of the Water Towers and Climate Change vehicles these are in lieu of standard pumping appliances.

It is worth noting that LFRS currently has several vehicles provided and maintained by Government under New Dimensions (5 Prime Movers and 1 Utility Terrain Vehicle), which under LFRS replacement schedules would be due for replacement during the period of the programme. However, our understanding is that Government will issue replacement vehicles if they are beyond economic repair, or if the national provision requirement changes. Should LFRS be required to purchase replacement vehicles, grant from Government may be available to fund them. Based on the current position, we have not included these vehicles (or any potential grant) in our replacement plan.

In addition, Fleet Services continue to review future requirements for the replacement of all vehicles in the portfolio, hence there may be some scope to modify requirements as these reviews are completed, and future replacement programmes will be adjusted accordingly. It is worth noting that as electric vehicles continue to develop we will consider the suitability of these for future replacements which, based on current price differentials, will increase the costs shown above.

Operational Equipment

With the exception of Body Armour all requirements are replacements for existing end of life equipment: Each of these groups of assets is subject to review prior to replacement, which may result in a change of requirements or the asset life.

Equipment Requirements (Cost per year)

Summary | 2023/24 £m | 2024/25 £m | 2025/26 £m | 2026/27 £m | 2027/28 £m |

|---|---|---|---|---|---|

Replacement of Existing Equipment | |||||

Thermal Imaging Cameras | 0.325 | – | – | – | – |

Breathing Apparatus (BA) and Telemetry equipment | – | – | 1.000 | 0.900 | 0.320 |

Cutting and extrication equipment | 0.750 | 0.750 | – | – | – |

Disposable Gas Tight suits | 0.042 | ||||

New Equipment | |||||

Body Armour | 0.250 | ||||

1.325 | 0.792 | 1.000 | 0.900 | 0.320 |

The replacement Breathing Apparatus project is in its early stages. Until such time as actual requirements in terms of type, numbers, telemetry and communications are known we will not be in a position to produce a more accurate cost or timing projection, however we currently anticipate some phasing of the implementation, hence costs are spread over 3 years. This may change as we progress through the project.

Body armour requirements are subject to a trial and hence requirements may change following the outcome of this.

ICT

The spend is on replacement/upgraded systems. All replacements identified in the programme will be subject to review, with both the requirement for the potential upgrade/replacement and the cost of such being revisited prior to any expenditure being incurred.

ICT Requirements (Cost per year)

Summary | 2023/24 £m | 2024/25 £m | 2025/26 £m | 2026/27 £m | 2027/28 £m |

|---|---|---|---|---|---|

Replace Existing Systems | |||||

Pooled PPE system | – | 0.100 | – | – | – |

Stock Management system | – | 0.100 | – | – | – |

Asset Management system | 0.100 | – | – | – | – |

HFSC referral system | 0.100 | – | – | – | – |

Fire Risk Management System | 0.100 | – | – | – | – |

Rota management package (WT/On call) | – | 0.100 | – | – | – |

Storage Area Network | – | 0.200 | 0.090 | – | – |

GIS Risk Info | – | 0.100 | – | – | – |

WAN | – | – | 0.450 | – | – |

IRS/MIS | – | – | 0.050 | – | – |

Firewall | 0.235 | – | – | – | – |

Wi-Fi | 0.135 | – | – | – | – |

New Operational Communications | |||||

Digitisation of Fire appliances – additional VMDS units | 0.254 | – | – | – | – |

Replace Operational Communications | |||||

ESMCP (Airwave replacement – assumed funded by grant) | – | – | 1.000 | – | – |

Incident Ground Radios | 0.230 | – | – | – | – |

UPS | – | – | – | – | 0.060 |

Total ICT Programme | 1.219 | 0.500 | 1.690 | – | 0.060 |

(Note HR & Payroll and the Finance system are both outsourced and form part of on-going SLAs, as such no allowance has been made for their future replacement, as it is assumed that any replacement costs are covered by the existing SLA. If at some point the Service moved away from the current SLAs, then we will incur costs in implementing new systems. We have not allowed for this).

Buildings

The only new scheme included in the above programme is Estate Improvements provision, which is a sum to enable us to make improvements to the estates on an on-going basis.

Building Requirements (Cost per year)

Summary | 2023/24 £m | 2024/25 £m | 2025/26 £m | 2026/27 £m | 2027/28 £m |

|---|---|---|---|---|---|

New Schemes | |||||

Estate Improvements | 0.250 | 0.250 | 0.250 | 0.250 | 0.250 |

Existing Schemes | |||||

Upgrade WYLFA Prop | 0.125 | ||||

W30 – Blackpool Welfare | 0.500 | – | – | – | – |

Drill tower replacements (notional 4 per year) | 0.600 | 0.600 | 0.600 | 0.600 | 0.600 |

C50 – Preston replacement station | – | 5.000 | 5.000 | – | – |

STC Props | – | 2.500 | 2.500 | – | – |

SHQ relocation | – | – | – | 7.500 | 7.500 |

1.475 | 8.350 | 8.350 | 8.350 | 8.350 |

In terms of all the building proposals it must be noted that we are still developing requirements/designs hence costings are indicative only.

The replacement of Preston Fire Station is subject to the outcome of a review of response provision within the Preston area and does not include any allowance for acquisition of a new site (should one be required), as it is assumed this will be offset by the sale of the existing site.

Th investment in Service Training Centre (STC) Props reflects the need to upgrade/replace some of the training props at STC which are nearing end of life.

The project to replace SHQ has been pushed back to 26/27, as a definitive decision on the project is required in order to further develop cost and timing. If the relocation does not go ahead, then we will need to review the existing provision and the need to undertake improvement works to ensure appropriate accommodation provision for the next 10 years.

The budget does not include any allowance for updating our property infrastructure to meet future Electric Vehicle charging requirements. This is estimated at £70k per site, but we need to develop a plan to roll out new electric vehicles in line with future regulations and modify sites to cope with this. It is unrealistic to implement this on a big bang approach, hence some phasing of this roll out will need to be incorporated into future capital programmes.

Total Capital Requirements

The following table details capital requirements over the five-year period:

Summary Capital Requirements

Summary | 2023/24 £m | 2024/25 £m | 2025/26 £m | 2026/27 £m | 2027/28 £m | Total £m |

|---|---|---|---|---|---|---|

Vehicles | 6.097 | 0.678 | 0.975 | 1.832 | 3.034 | 12.616 |

Operational Equipment | 1.325 | 0.792 | 1.000 | 0.900 | 0.320 | 4.337 |

IT Equipment | 1.219 | 0.500 | 1.690 | – | 0.060 | 3.469 |

Buildings | 1.475 | 8.350 | 8.350 | 8.350 | 8.350 | 34.875 |

10.116 | 10.320 | 12.015 | 11.082 | 11.764 | 55.297 |

Capital Funding

Capital expenditure can be funded from the following sources:

Prudential Borrowing

The Prudential Code gives the Authority increased flexibility over its level of capital investment and much greater freedom to borrow, should this be necessary, to finance planned expenditure. However, any future borrowing will incur a financing charge against the revenue budget for the period of the borrowing.

Given the financial position of the Authority we have not needed to borrow since 2007 and repaid a large proportion of our borrowing in October 2017.

Capital Grant

Capital grants are received from other bodies, typically the Government, in order to facilitate the purchase/replacement of capital items.

There is an expectation that the ESMCP project costs will be offset by capital grant, however we have not had any confirmation of this.

To date no other capital grant funding has been made available, nor has any indication been given that capital grant will be available in future years, and hence no allowance has been included in the budget.

Capital Receipts

Capital receipts are generated from the sale of surplus property and vehicle assets, with any monies generated being utilised to fund additional capital expenditure either in‑year or carried forward to fund the programme in future years.

The Authority expects to hold £1.7m of capital receipts as at 31 March 2023. This will be fully utilised during the 5-year programme.

It is worth highlighting that the relocation of SHQ would provide an opportunity to sell part or all of the site, subject to any changes at Fulwood Fire Station, however any sale proceeds will not be realised within the timeframe of this programme.

Capital Reserves

Capital Reserves have been created from under spends on the revenue budget in order to provide additional funding to support the capital programme in future years. The Authority expects to hold £18.6m of capital reserves as at 31 March 2023. Over the life of the programme we anticipate utilising all these reserves.

Revenue Contribution to Capital Outlay (RCCO)

Any revenue surpluses may be transferred to a Capital Reserve in order to fund additional capital expenditure either in‑year or carried forward to fund the programme in future years.

As referred to in the Revenue Budget report, elsewhere on this agenda, the revenue contribution to capital is currently set at £4.0m per year, giving total funding of £20.0m over the 5 years. This reduces the need to borrow and hence the capital financing charge associated with this.

Drawdown of Earmarked Reserves

£0.4m has been drawn down from the Innovation Reserve/Earmarked Reserve to fund the digitisation of fire appliances project and part of the WYLFA prop upgrade.

Drawdown of General Reserves

No allowance has been made for the drawdown of any of the general reserve.

Total Capital Funding

The following table details available capital funding over the five-year period:

Table 8 Summary Capital Funding

2023/24 | 2024/25 | 2025/26 | 2026/27 | 2027/28 | TOTAL | |

£m | £m | £m | £m | £m | £m | |

Capital Grant | – | – | 1.000 | – | – | 1.000 |

Capital Receipts | 1.683 | – | – | – | – | 1.683 |

Capital Reserves | 4.069 | 6.320 | 7.015 | 1.197 | – | 18.601 |

Earmarked Reserves | 0.364 | – | – | – | – | 0.364 |

Revenue Contributions | 4.000 | 4.000 | 4.000 | 4.000 | 4.000 | 20.000 |

10.116 | 10.320 | 12.015 | 5.197 | 4.000 | 41.648 |

Summary Programme

Based on the draft capital programme as presented we have a shortfall of £13.6m:

Summary Capital Requirements and Funding Available

Summary | 2023/24 £m | 2024/25 £m | 2025/26 £m | 2026/27 £m | 2027/28 £m | Total £m |

|---|---|---|---|---|---|---|

Capital Requirements | 10.116 | 10.320 | 12.015 | 11.082 | 11.764 | 55.297 |

Capital Funding | 10.116 | 10.320 | 12.015 | 5.197 | 4.000 | 41.648 |

Surplus/(Shortfall) | – | – | – | (5.885) | (7.764) | (13.649) |

This show there is a significant funding gap.

Impact on the Revenue budget

The capital programme shows the Authority utilising all of its capital reserves and receipts part way through 2026/27, meaning that the remainder of the capital programme will need to be met from either capital grant (if available), additional revenue contributions or from new borrowing.

The draft budget as set out shows a need to borrow £13.6m. As we have already set aside £2.0m of funds, this would entail £11.6m of new borrowing. This has a significant impact on the revenue budget, in terms of interest payments and setting aside a sum equivalent to the Minimum Revenue Provision (MRP), as shown in the table below. (Note both the interest rate and the life over which MRP is charged are subject to change.)

Cost of Borrowing

Summary | 26/27 Impact | 27/28 Impact |

|---|---|---|

Interest per annum | £88k | £350k |

MRP (MRP is only charged in year after purchase) | – | £118k |

Total | £88k | £468k |

The cost of this borrowing is incorporated into the revenue budget in future years, but the full year effect of this borrowing will not be felt until 28/29, where the total cost would be £0.8m.

Programme Assumptions

It is also worth highlighting that the programme is based around a number of assumptions which could change:

All costings are subject to refinement during the design and procurement phases;

Vehicle replacements are based on the Fleet Asset management Plan, however the scale of replacements in 23/24 is extremely high and hence some slippage is likely, furthermore whilst we have extended the life of appliances to 13 years a review of our scope to extend this further is underway;

New Dimensions vehicle replacements are expected to be carried out by Government; however this position may change;

No allowance has been made for developments in operational equipment, which may justify future investments. At the present time this would need to be met from the Innovation reserve, of which we have £0.25m remaining, or from the revenue budget;

ICT software replacements are subject to review prior to replacement, which has led in the past to significant slippage;

Operational Communications replacements (ESMCP) are subject to a great deal of uncertainty in terms of both timing and costs as they are related to a national replacement project, in addition there may be grant funding available for this which is also unknown at this time;

The costs and timing for replacement of Preston Fire Station, investment in STC Props and relocation of SHQ are estimates only at this stage;

Capital grant may be made available in future years, in order to assist service transformation and greater collaboration, although this is felt to be unlikely.

Summary

Without borrowing the current programme is not balanced, as such the Authority will need to borrow £11.6m over the life of the programme. The cost of this borrowing is incorporated into the revenue budget, however this only impacts the last year of the Medium Term Financial Strategy. Given this the Treasurer considers that the programme is prudent, sustainable and affordable in the medium term.

As noted above, should any of the funding assumptions or expenditure items within the programme change, this will have an impact on the overall affordability of the programme.

Prudential Indicators

The Prudential Code gives the Authority increased flexibility over its level of capital investment and much greater freedom to borrow, should this be necessary, to finance planned expenditure. However, in determining the level of borrowing, the Authority must prepare and take account of a number of Prudential Indicators aimed at demonstrating that the level and method of financing capital expenditure is affordable, prudent and sustainable. These Indicators are set out at Appendix 1, along with a brief commentary on each. The Prudential Indicators are based on the programme set out above. These indicators will be updated to reflect the final capital outturn position and reported to the Resources Committee at the June meeting.

The main emphasis of these Indicators is to enable the Authority to assess whether its proposed spending and its financing is affordable, prudent and sustainable and in this context, the Treasurer’s assessment is that, based on the indicators, this is the case for the following reasons:

In terms of prudence, the level of capital expenditure, in absolute terms, is considered to be prudent and sustainable at an annual average of £10.5m over the 3-year period. The trend in the capital financing requirement and the level of external debt are both considered to be within prudent and sustainable levels. Whilst new borrowing is required this only occurs in the last two years of the programme.

In terms of affordability, the negative ratio of financing costs is attributable to interest receivable exceeding interest payable and Minimum Revenue Provision payments in each of the three years. This reflects the effect of the previous decision to set aside monies to repay debt.

Capital Expenditure and Financing

The objective in consideration of the affordability of the Authority’s capital plans is to ensure that total capital expenditure remains within sustainable limits.

Capital expenditure 2021/22 to 2025/26

The actual expenditure for 2020/21 and forecast expenditure 2021/22, and estimates of capital expenditure to be incurred in future years, as per the proposed capital programme and allowing for slippage from the 2021/22 programme, are:

Capital expenditure by year

Summary | 2021/22 Actual £m | 2022/23 Forecast £m | 2023/24 Estimate £m | 2024/25 Estimate £m | 2025/26 Estimate £m |

|---|---|---|---|---|---|

Capital Expenditure | 3.350 | 3.271 | 10.116 | 10.320 | 12.015 |

This indicator for 2022/23 will also be updated at the year-end to reflect actual capital expenditure incurred.

Capital financing 2021/22 to 2025/26

All capital expenditure must be financed, either from external resources (government grants and other contributions), the Authority’s own resources (revenue contributions, reserves and capital receipts) or debt (borrowing, leasing and Private Finance Initiative). The planned financing of the above expenditure is as follows:

Capital financing by year

Summary | 2021/22 Actual £m | 2022/23 Forecast £m | 2023/24 Estimate £m | 2024/25 Estimate £m | 2025/26 Estimate £m |

|---|---|---|---|---|---|

Grants and Contributions | – | – | – | – | 1.000 |

Own Resources | 3.350 | 3.271 | 10.116 | 10.320 | 11.015 |

Debt | – | – | – | – | – |

Total | 3.350 | 3.271 | 10.116 | 10.320 | 12.015 |

Borrowing Strategy

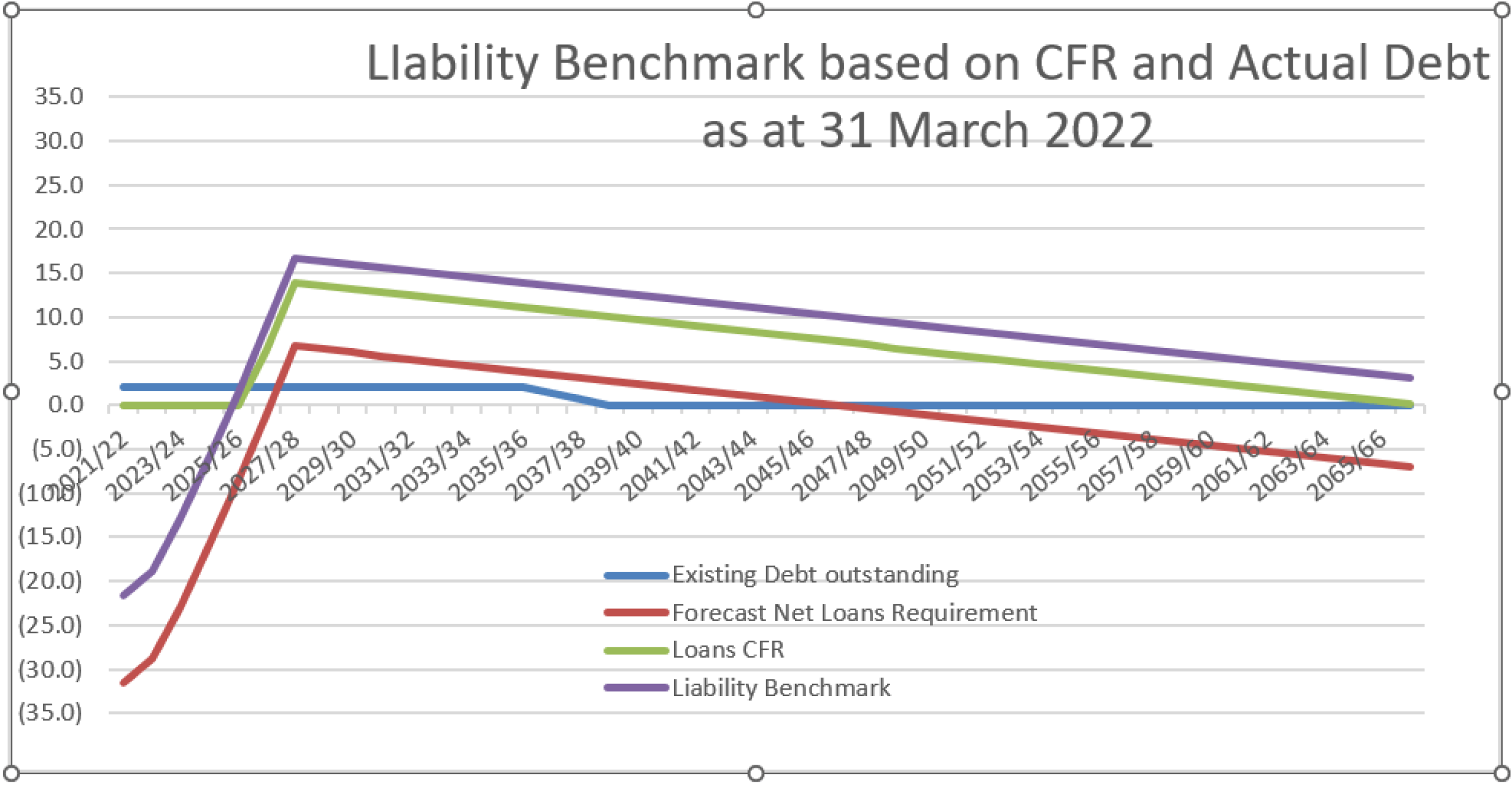

Capital Financing Requirement (CFR) 2021/22 to 2025/26

Capital financing requirements by year

Summary | 2021/22 Actual £m | 2022/23 Forecast £m | 2023/24 Estimate £m | 2024/25 Estimate £m | 2025/26 Estimate £m |

|---|---|---|---|---|---|

Capital Financing Requirement (Debt only) | – | – | – | – | – |

The capital financing requirement measures the authority’s underlying need to borrow for a capital purpose and reflects the effects of previous investment decisions as well as future planned expenditure. In accordance with best professional practice, the Authority does not associate borrowing with particular items or types of expenditure. External borrowing arises as a consequence of all the financial transactions of the Authority and not simply those arising from capital spending, but in the medium term the Treasurer anticipates that borrowing is undertaken for capital purposes only. These capital financing requirements then feed through into the anticipated level of external debt as reported in the Treasury Management Strategy elsewhere on the agenda but repeated here for completeness. As reported in the Treasury Management Strategy the Authority has made additional MRP provisions since 2010/11 in order to reduce capital financing requirements to nil.

Authorised limit and operational boundary for its total external debt

In respect of its external debt the Authority is required to set two limits over the three-year period: an authorised limit and an operational boundary. Both are based on the planned capital expenditure, estimates of the capital financing requirement and estimates of cash flow requirements for all purposes. It should be noted that these limits have then been uplifted to include potential borrowing associated with a future decision to go ahead with a replacement Headquarters.

The operational boundary is based on the most likely, but not worst case, scenario and represents the maximum level of external debt projected by these estimates. However, unexpected cashflow movements can occur during the year and some provision needs to be made in setting the authorised limit to deal with this.

The two indicators are as follows:

Borrowing Limits by year

Summary | 2021/22 Actual £m | 2022/23 Forecast £m | 2023/24 Estimate £m | 2024/25 Estimate £m | 2025/26 Estimate £m |

|---|---|---|---|---|---|

Authorised Limit for External Debt | |||||

Borrowing | 6,000 | 4,000 | 4,000 | 4,000 | 4,000 |

Other long-term liabilities | 30,000 | 30,000 | 30,000 | 30,000 | 30,000 |

Total | 36,000 | 34,000 | 34,000 | 34,000 | 34,000 |

Operational Boundary for External Debt | |||||

Borrowing | 3,000 | 3,000 | 3,000 | 3,000 | 3,000 |

Other long-term liabilities | 17,000 | 16,000 | 16,000 | 16,000 | 15,000 |

Total | 20,000 | 19,000 | 19,000 | 19,000 | 18,000 |

Gross debt and the Capital Financing Requirement

The Prudential Code requires that debt does not exceed the Capital Financing Requirement except in the short term, in order to ensure that over the medium term that debt will only be for capital purposes. This is a key indicator of prudence.

As reported in the Treasury Management Strategy, the Authority has made additional MRP provisions since 2010/11 in order to reduce Capital Financing Requirements and hence the charges associated with this, and in order to set monies aside to pay off debt as it matures. It used these monies to pay off £3.2m of debt in October 2017. As a result of this the level of debt now held, £2.0m, exceeds the capital financing requirement, has been zero after MRP payments made during 2019/20: –

Table 16 Debt and the Capital Financing Requirements by year

Summary | 2021/22 Actual £m | 2022/23 Forecast £m | 2023/24 Estimate £m | 2024/25 Estimate £m | 2025/26 Estimate £m |

|---|---|---|---|---|---|

Debt | 2.000 | 2.000 | 2.000 | 2.000 | 2.000 |

Capital Financing Requirement | – | – | – | – | – |

Revenue Budget Implications

Although capital expenditure is not charged directly to the revenue budget, interest payable on loans and Minimum Revenue Provision (MRP, or debt repayments) are charged to revenue, offset by interest receivable. The net annual charge is known as financing costs.

As shown within the Treasury Management Strategy report elsewhere on the agenda, the financing costs are as follows:

Impact on Revenue Budget by year

Summary | 2021/22 Actual £m | 2022/23 Forecast £m | 2023/24 Estimate £m | 2024/25 Estimate £m | 2025/26 Estimate £m |

|---|---|---|---|---|---|

Interest payable | 0.090 | 0.090 | 0.090 | 0.090 | 0.090 |

MRP | 0.010 | 0.010 | – | – | – |

Interest receivable | (0.206) | (0.770) | (1.300) | (1.000) | (0.650) |

Net financing costs | (0.106) | (0.680) | (1.210) | (0.910) | (0.560) |

Proportion of financing costs to net revenue stream

Proportion of financing costs to net revenue stream by year

Summary | 2021/22 Actual £m | 2022/23 Forecast £m | 2023/24 Estimate £m | 2024/25 Estimate £m | 2025/26 Estimate £m |

|---|---|---|---|---|---|

Net financing costs | (£0.106m) | (£0.680m) | (£1.210m) | (£0.910m) | (£0.560m) |

Ratio of Financing Costs to Net Revenue Stream | (0.18%) | (1.08%) | (1.85%) | (1.28%) | (0.76%) |

The negative percentage of this indicator reflects the low level of underlying debt (following the repayment of the majority of our long-term loans during 2017/18) for the Authority in comparison to the authority’s level of investment income, i.e. interest receivable is significantly higher than interest payable.

Section 3: Reserves and Balances

Reserves and Balances Policy 2023/24-2027/28

The National Framework includes a section on reserves. The main components of which are:

General reserves should be held by the fire and rescue authority and managed to balance funding and spending priorities and to manage risks. This should be established as part of the medium-term financial planning process.

Each fire and rescue authority should publish their reserves strategy on their website. The reserves strategy should include details of current and future planned reserve levels, setting out a total amount of reserves and the amount of each specific reserve that is held for each year. The reserves strategy should provide information for at least two years ahead.

Sufficient information should be provided to enable understanding of the purpose for which each reserve is held and how holding each reserve supports the fire and rescue authority’s medium-term financial plan.

Information should be set out in a way that is clear and understandable for members of the public, and should include:

¬ how the level of the general reserve has been set;

¬ justification for holding a general reserve larger than five percent of budget;

¬ whether the funds in each earmarked reserve are legally or contractually committed, and if so, what amount is so committed; and

¬ a summary of what activities or items will be funded by each earmarked reserve, and how these support the fire and rescue authority’s strategy to deliver good quality services to the public.

The reserves policy complies with these requirements.

General Reserves (General Fund)

These are non-specific reserves which are kept to meet short/medium term unforeseeable expenditure and to enable significant changes in resources or expenditure to be effectively managed in the medium term.

The Authority needs to hold an adequate level of general reserves to provide:

A working balance to help cushion the impact of uneven cash flows and avoid unnecessary temporary borrowing;

A contingency to cushion the impact of unexpected events;

A means of smoothing out large fluctuations in spending requirements and/or funding available.

The following table sets out the purpose of this reserve, how it is utilised, controlled and reviewed.

Summary of General Reserves (General Fund)

Name | General Reserves (General Fund) |

|---|---|

Purpose | This covers uncertainties in future years budgets, such as:

|

Utilisation | This is utilised to offset any in-year overspend that would occur when comparing budget requirement to the level of funding generated. |

Controls | The utilisation of this is agreed as part of the annual budget setting process. Any further utilisation requires the approval of the Resources Committee. |

Review | The adequacy of this is reviewed annually, as part of the budget setting process. |

Review of Level of Reserves

In determining the appropriate level of general reserves required by the Authority, the Treasurer is required to form a professional judgement on this, taking account of the strategic, operational and financial risk facing the Authority. This is completed based on guidance issued by CIPFA and includes an assessment of the financial assumptions underpinning the budget, the adequacy of insurance arrangements and consideration of the Authority’s financial management arrangements. In addition, the assessment should focus on both medium and long-term requirements, taking account of the Medium-Term Financial Strategy (MTFS) (as set out in the draft budget report elsewhere on this agenda).

For Lancashire Combined Fire Authority this covers issues such as: uncertainty surrounding future funding settlements and the potential impact of this on the revenue and capital budget; uncertainty surrounding future pay awards and inflation rates; the impact of changes to pension schemes and the remedy for the McCloud judgement; demand led pressures; risk of default associated with our investments, cost associated with maintaining operational cover in the event of Industrial Action etc.

There remains a great deal of uncertainty over long term funding, as a result, the anticipated multi-year settlement has been postponed again. The Local Government Finance Settlement only covered 2023/24, although the policy statement that accompanied it stated “The core settlement will continue in a similar manner for 2024-25. The major grants will continue as set out for 2023-24: Revenue Support Grant will continue and be uplifted in line with Baseline Funding Levels”. Whilst this provides a basis for estimating future funding increases, as set out in the revenue budget paper, it does not provide any certainty.

Furthermore, the outcome of the fair funding review of relative needs and resources and the Government intention to move to greater retention of Business Rates have also been postponed.

The position in terms of pay awards has still not been resolved, however the likelihood of this being significantly higher than the budgetary allowance and the likelihood of industrial action have both reduced as a result of the latest pay offer.

Whilst future pension costs remain uncertain, with Authorities still awaiting definitive guidance on how to implement changes following the McCloud judgement, and with the next revaluation of the FF pension scheme being due this year, the draft budget for 24/25 already includes a 3% allowance for this.

As such the Treasurer considers it prudent to reduce the minimum target reserves level to £3.75m, 5.5% of the 2023/24 net revenue budget, reflecting the level of uncertainty. (Note, it may be possible to reduce this minimum level further if the current grey book 2 year pay offer is accepted.) This is slightly higher than the 5% threshold identified by the Home Office above which the Authority is required to justify why it holds the level of reserves, reflecting the increasing uncertainty about future funding, pension costs and pay awards.

Should reserves fall below this minimum level the following financial year’s budget will contain options for increasing reserves back up to this level. (Note, this may take several years to achieve.)

Whilst this exercise sets a minimum level of reserves it does not consider what, if any, maximum level of reserves is appropriate. In order to do this the level of reserves held should be compared with the opportunity cost of holding these, which in simple terms means that if you hold reserves that are too high you are foregoing the opportunity to lower council tax or invest in further service improvements.

Whilst the settlement provides greater flexibility to increase council tax in 23/24, this is a one-off relaxation of the referendum principles and current indications are that it will not be repeated in future years. Hence the scope to increase council tax in future years to restore depleted reserves is limited, without holding a local referendum. Therefore, any maximum reserve limit must take account of future anticipated financial pressures and must look at the long-term impact of these on the budget and hence the reserve requirement. Based on professional judgement, the Treasurer feels that this should be maintained at £10.0m.

Should this be exceeded the following financial year’s budget will contain options for applying the excess balance in the medium term, i.e. over 3-5 years.

Level of General Reserves

The overall level of the general fund balance, i.e., uncommitted reserves, anticipated at the 31 March 2023 is £4.0m, providing scope to utilise approx. £0.25m of reserves.

The draft budget as presented elsewhere on the agenda identifies a funding gap of £0.3m in 23/24, which could be me from a combination of a drawdown against this reserve and additional in-year savings. The Treasurer therefore considers this reserve is at an appropriate level.

Looking at the medium term the need to drawdown reserves will be affected by:

Council tax – The revenue budget assumes that council tax is increased by the maximum permissible each year, enabling the Service to deliver a balanced budget each year, after allowing for relatively low level of reserve drawdown/additional savings. If this is not the case, then we may need to utilise reserves in future years to balance the budget.

Pension costs – the revenue budget assumes that the only pension costs that fall on the Service are employer contributions, and that all other costs are met by the Government via the Pension Holding Account. If this is not the case, then reserves would be required to meet these one-off costs which will be very significant. Furthermore it assumes that the employer contribution rate will increase by 3% following the next tri-annual revaluation exercise, but at the present time no details are available hence contribution rates could increase by a greater amount.

Future funding – The revenue budget assumes future funding increases by 5% in 24/25 followed by 2% increases thereafter. If that is not the case and it is frozen as part of the next mufti-year settlement, this would reduce funding levels by £0.6m each year, a cumulative reduction of £1.9m over the medium-term financial strategy, and this would impact on the need to drawdown reserves

Future inflation – The revenue budget assumes pay awards running at 5% in 23/24 before returning to the Government’s 2% target. If this is not the case each 1% more than this increases the recurring budget requirement by £0.4m, i.e. £2.9m over the next 5 years, which may impact on the usage of reserves.

At the present time, the MTFS identified funding gaps in the next 4 years. Assuming 50% of these are met by additional in-year savings with the balances being drawdown form this reserve, we will potentially see this reserve falling to £3.2m by March 27. This is below our current minimum requirement. However the forecasts are subject to a number of variable factors , as set out above, and these will continue to be reviewed to refine forecasts and ensure that reserves remain above our minimum threshold throughout the duration of the MTFS.

Earmarked Reserves

These are reserves created for specific purposes to meet known or anticipated future liabilities and as such are not available to meet other budget pressures. They can only be used for that specific purpose, for which they were established, and as such it is not appropriate to set any specific limits on their level, but as part of the annual accounts process their adequacy will be reviewed and reported on.

The following table sets out the purpose of this reserve, how it is utilised, controlled and reviewed.

Summary of Earmarked Reserve

Name | Earmarked |

|---|---|

Purpose | This covers monies set aside for specific purposes. |

Utilisation | Once set up these reserves can only be used for the specific purpose for which they were established. |

Controls | The utilisation of these are discussed at quarterly DFM meetings between the budget holder, relevant Executive Board member, and the Director of Corporate Services. |

Review | The level of earmarked reserves is reviewed each year as part of the revenue outturn/annual accounts process to ensure these are reasonable and remain relevant. |

The Director of Corporate Services has delegated authority to create new earmarked reserves valued at up to £100,000; any request which exceeds this must be reported to the Resources Committee for approval.

Specific earmarked reserves will be closed when there is no longer a requirement to hold them, at which point they will either hold a nil balance or when any outstanding balance will be transferred into the general reserve.

Level of Earmarked Reserves

The following table provides a breakdown of the £2.6m of earmarked reserves forecast to be held at 31st March 2023, and a forecast of the anticipated position as at 31 March 2028:

Table 4 Earmarked Reserve Balances

Summary | Forecast at 31 March 2023 £m | Forecast at 31 March 2028 £m | Notes |

|---|---|---|---|

Specific Grant C/Fwd. | 0.2 | – | This reserve carries forward unspent specific grants

We anticipated utilising these in the new financial year. There are no contractual or legal obligations against this reserve |

DFM Reserve | 0.3 | 0.3 | Devolved Financial Management Reserve enables budget holders to carry forward any surplus or deficit from one financial year to the next, within prescribed limits. This reserve provides greater flexibility to individual budget holder to carry forward underspends within their own budget area to meet future costs and optimise the use of resources. Examples of areas where these balances have been used previously would-be one-off replacements of equipment, or enhancement to station facilities etc. The levels of individual DFM reserves are reviewed each year as part of the revenue outturn/annual accounts process, to ensure that they are reasonable and that budget holders are not building up excessive reserves. As a result of this exercise we have stripped out £0.1m and transferred this into the capital funding reserve (referred to later in the report) At present there are no contractual or legal obligations against this reserve, as any such commitments would be included in the base revenue budget. |

Insurance Aggregate Stop Loss (ASL) | 1.1 | 1.1 | The Authority has aggregate stop losses (ASLs) on both its combined liability insurance policy (£0.4m) and its motor policy (£0.3m). This means that in any one year the Authority’s maximum liability for insurance claims is capped at the ASL. As such the Authority can either meet these costs direct from its revenue budget or can set up an earmarked reserve to meet these. Within Lancashire we have chosen to meet the potential costs through a combination of the two. Hence the amount included in the revenue budget reflects charges in a typical year, with the reserve being set up to cover any excess over and above this. As such the reserve, combined with amounts within the revenue budget, provides sufficient cover to meet 2 years’ worth of the maximum possible claims, i.e. the ASL. (It is worth noting that the revenue budget allocation has also been reduced in recent years reflecting the claims history. Without holding this reserve to cushion any major claims that may arise this would not have been possible.) None of this reserve is legally committed at the present time, although as soon as a claim arose this position would change. |

Prince’s Trust | 0.4 | 0.4 | This reserve has been established to balance short term funding timing differences and to mitigate the risk of loss of funding and enable short term continuation of team activities, whilst alternative funding is found. Without this reserve any significant loss of funding would have an immediate impact on our ability to deliver the PT programme, and hence improve the lives of younger people. This reserve has been capped at £0.5m. There are no legal or contractual commitments against this, however forecasts show this budget reducing reflecting the uncertainty over future funding |

Apprentices | 0.1 | – | This reserve was created from previous in-year underspends relating to the appointment of apprentices, which was delayed awaiting national developments. As such the reserve was set up to offset some of the pay/training costs that will be incurred in future years, with the balance being met direct from the revenue budget. This clearly contributes to addressing apprenticeship targets, set by the Government, as well as addressing capacity issues within departments. There are no contractual commitments against this. |